The survival of a startup is determined by its ability to create something of value that enough people will pay for, before running out of steam (financially and emotionally).

There's a method for creating value. The better you understand it, the better your ability to achieve it. We'll explore Value Creation in this two-part blog series.

The overall objective of a business is creating something of enough value that people will pay for it. And fast.

The science behind turning an idea into a business is identifying what variables will create something that generates sufficient revenue.

Real v. Perceived Value

Before we get into it, it's important to distinguish between real value and perceived value. When you're considering the overall value of your product, you should understand both the real and perceived value.

Real value refers to:

- How much it costs to produce the product

- How useful it is to the buyer

- How much value it's individual components have

Drivers include production inputs and how big of a problem the product solves for the customer.

Perceived value is a more abstract measurement that represents how much customers feel a product is worth. Additional drivers (in addition to the real value of the product) include:

- Marketing and sales efforts

- Startup DNA (Vision, Mission, Values, Philosophy etc)

- Brand and customer experience

Your customer's perception of the value of your product determines their willingness to buy it at a particular price, so we use Perceived Value as the measure of ultimate value to the customer.

Value Relationships

Note that this an expression of the variables that drive value, designed as a decision making and optimisation tool.

Fundamental Truths:

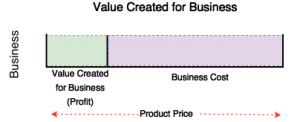

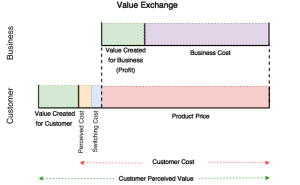

For a business to be sustainable, it needs to make and sell a product that provides enough value that customers are willing to pay a price (Product Price) that is higher than what it costs to make and sell the product (Business Cost).

And, for a customer to buy something, the value perceived by the customer (Perceived Value) needs to be higher than what it cost the customer to acquire and use the product (Customer Cost).

So,

- Product Price > Business Cost

- Perceived Value > Customer Cost

Where,

- Product Price = How much money you can sell the product for

- Business Cost = The total cost per unit (includes the cost of producing and selling the product plus operating cost per unit)

- Perceived Value = The value that a customer assigns to your product

- Customer Cost = The cost to the customer to acquire and use your product

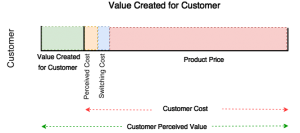

Customer Cost:

Customer Cost includes:

- Money (Product Price)

- Time and effort required to start using the new product (Switching Costs)

- Any perceived risks associated with buying and using the product (Perceived Costs).

Switching Costs includes behavioural changes that are required to acquire and use your product, including the forming new habits, and the time and effort it takes to sign up, on board, login, travel to the destination etc.

Perceived Costs take into consideration the emotional impact of buying and using the product (fears). For example, how will customers look to their peer group using your product? How will their boss or colleagues respond? How reliable is your product or company? What will happen if they want to get their money out? Are you trustworthy? Will they feel guilty after purchasing the product?

Existing Alternatives

When there are existing alternatives, the difference between the Perceived Value of your product and Customer Cost, needs to be greater than that of your competitors.

For your customer to choose your product over existing alternatives,

Perceived value of product - Customer Cost for product > Perceived Value of existing alternative - Customer Cost for existing alternative.

The Value Exchange

When a product is bought or sold there is a value exchange between the customer and the business. In this process, new value is created.

Value Created for Business - The value to the business is equal to the value the business receives minus the cost of creating and selling the product:

Created Value (Business) = Product Price - Cost of Sale

Created Value (Business) = Product Price - Cost of Sale

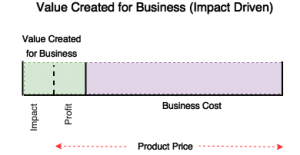

Or, where your business is not only optimising for profit:

Created Value to Business = Business Percieved Value- Cost of Sale

Where:

Product Value (Business) = Product Price + Non-monetary Value.

Non-monentary value can include social impact.

For simplicities sake, we will assume that Business Value = Product Price.

Value Created for Customer

The additional value a customer gets from your product is equal to benefits they get minus the cost of gaining these benefits. This is the additional value that has been created for your customer by purchasing your product.

Created Value (Customer) = Customer Perceived Value - Customer Cost

For the customer, the more value created the better, as any individual is trying to optimise the value they get from their time or money investments. The higher they perceive this gain to be, the more willing they will be to buy and keep using your product.

Created Value (Customer) = Customer Perceived Value - (Product Price - Switching Costs - Perceived Costs)

The Fair Value Exchange - A Hypothesis

In an equal value exchange, which arguably is a sustainable model:

Created Business Value = Created Customer Value

i.e. the amount of additional benefit that the customer gets from the product is equal to the additional value the business gets (either through the price the customer pays or through non-monetary benefits).

What happens a company is not in equilibrium:

- Value Created for Business > Value Created for Customer - there is an opportunity for someone to do what you do better. In theory, someone else can use the same resources as you at turn it into something that provides more relative value for your customer. The bigger the imbalance, the more opportunity there is for competition or disruption.Obvious examples of this can be seen with banks and other large corporates that charge significant fees and don't appear to provide a high enough value to their customers in return, as they focus on maximising return to their shareholders instead.

- Value Created for Customer > Value Created for Business - less sustainable long term as the business does not have the optimal resources to maintain competitive in terms of attracting and maintaining the best people (employees, investors etc), the best product and the best environment.

The 'value equilibrium' is something that would be near impossible to perfect, given that there are so many variables that can't accurately be measured, just like most economic equilibriums. The best way for companies to work towards this hypothetical equilibrium is to have a core set of values that provides a guideline for where value is assigned

The application of these concepts:

Part 1 covers the theory behind this concept. We cover about the practical application of this concept and how to optimise value in Part 2. This includes top tips that you can apply to your startup development >>